Credit card debt is at record highs, and knowing when to pay your credit card bill can make a meaningful difference in both the interest you pay and your credit score.

While many people focus only on the due date, understanding the full credit card billing cycle can help you optimize your payments and improve your financial health.

Why Timing Matters

Your credit score is influenced by several factors, including payment history (35%) and credit utilization (30%). Both are directly impacted by when and how you make payments.

Pay Attention to Your Credit Utilization Rate

Credit utilization measures how much of your available credit you are using. Experts generally recommend keeping your usage below 30% of your credit limit.

For example, if your credit limit is $10,000, try not to carry more than $3,000 during a statement period. While some believe 30% is the goal, it’s better viewed as a soft ceiling.

At the same time, a 0% utilization rate can signal inactivity, which may not help your credit profile. Responsible usage and timely payments show lenders that you can manage credit wisely.

The Three Important Dates

- Statement Date: The day your card issuer calculates your monthly balance.

- Due Date: The deadline to make at least the minimum payment.

- Reporting Date: When your balance is reported to credit bureaus.

Paying on or before your due date protects your payment history. However, paying shortly after your statement date can improve your utilization ratio before it gets reported.

How Early Payments Reduce Interest

Credit card interest is calculated based on your average daily balance. Paying earlier in your billing cycle reduces your average balance and lowers the interest charged.

For example, paying half your balance mid-cycle instead of on the due date can noticeably reduce interest costs over time.

So When Is the Absolute Best Time?

The optimal strategy is:

- Keep usage under 30% of your limit

- Pay most or all of your balance right after your statement posts

- Always pay at least the minimum by the due date

- Consider early payments to reduce interest

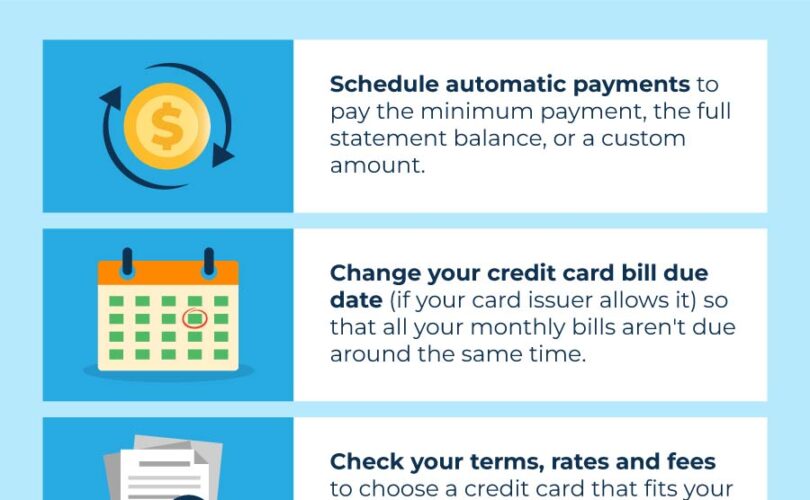

Auto-Pay Is Your Friend

Setting up automatic payments ensures you never miss a due date. If possible, automate at least the minimum payment and manually pay additional amounts earlier in the cycle.

Final Thoughts

Understanding your statement date, due date, and reporting date gives you a strategic advantage. Small adjustments in timing can protect your credit score and reduce interest costs.

Disclaimer

The content provided on MoneyMentor is for educational purposes only and does not constitute tax, legal, or investment advice. Financial decisions should be made with guidance from a qualified professional.