If you have take-home pay of, say, $3,000 a month, how can you pay for housing, food, insurance, health care, debt repayment and fun without running out of money? That’s a lot to cover with a limited amount.

The answer is to make a budget.

What is a budget? A budget is a plan for every dollar you have. Using your take-home pay as a starting point, a budget organizes your expenses, savings goals and other financial obligations into a manageable system that can provide more financial freedom and a less stressful life.

How to budget money

It’s easy to get overwhelmed by the many details included in the budgeting process. Here are five steps to follow.

Step 1. Figure out your after-tax income

If you get a regular paycheck, the amount you receive is probably your after-tax income, but if you have automatic deductions for a 401(k), savings, and health and life insurance, add those back in to give yourself a true picture of your savings and expenditures. If you have other types of money coming in — such as from side gigs — subtract anything that reduces that income, such as taxes and business expenses. Figure out your net income using our nifty calculator.

Step 2. Choose a budgeting system

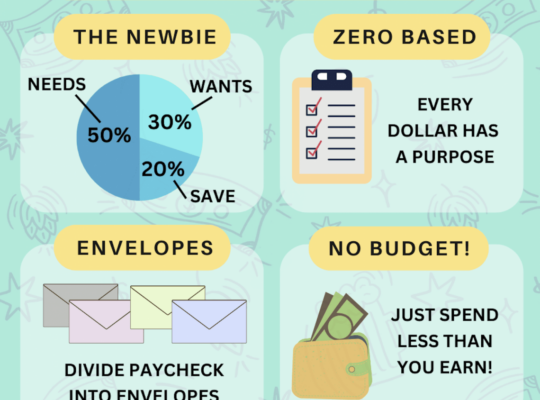

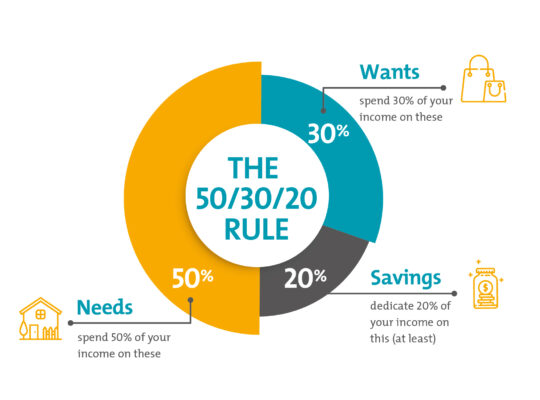

A budgeting system is a framework for how you budget. Everyone has different habits, personality types and approaches to managing money, and there are systems that can fit your lifestyle. Any budget must cover all of your needs, some of your wants and — this is key — savings for emergencies and the future. Budgeting system examples include the envelope system, the zero-based budget, and the 50/30/20 budget, which we’ll discuss more below.

Step 3. Track your progress

Record your spending or use online budgeting and savings tools. During this step, it’s important to pay attention to where your money is going. If you notice areas where you’re overspending, consider cutting those costs. The money you notice slipping through the cracks could go toward debt repayment, savings or another financial priority.

Step 4. Automate your savings

Automate as much as possible so the money you’ve allocated for a specific purpose gets there with minimal effort on your part. If your employer permits, set up automatic payments from your paycheck to your emergency savings, investment and retirement accounts. An accountability partner or online support group can help, so that you’re held accountable for choices that don’t fit the budget.

Step 5. Practice budget management

Your income, expenses and priorities will change over time, so manage your budget by revisiting it regularly, perhaps once a quarter. If you find that the initial budgeting system you choose isn’t working for you, consider trying a different strategy. The budget you choose doesn’t have to last forever.