Learn about the different behaviors that can raise or lower an individual’s score, such as the length of credit history, frequency of credit inquiries, and overall debt-to-credit ratio.

Related

Raising your credit score

There are several things you can do to raise your credit score:

Pay your bills on time

Late payments can have a negative impact on your credit score, so it’s important to pay all your bills on time and in full whenever possible.

Keep your credit utilization low

Your credit utilization is the percentage of your available credit that you’re using. For example, if you have a credit card with a $1,000 limit and you’re using $500 of it, your credit utilization is 50%. If you’re using more than 30% of your available credit, it can hurt your credit score.

Monitor your credit report

Keep an eye on your credit report to make sure there aren’t any errors that could be hurting your score. If you find any inaccuracies, be sure to dispute them right away.

Build a longer credit history

Your credit score is partly based on how long you’ve been using credit. So, the longer you have a credit history, the better. Do not close any credit accounts, even if you have not used them in a while.

Avoid applying for too many new credit accounts

Every time you apply for a new credit account, your credit score takes a small hit. If you apply for multiple new accounts in a short period of time, it can add up and impact your score.

Keep a mix of credit types

Having different types of credit (like a mortgage, car loan, and credit card) can show that you’re able to manage different types of debt, which can boost your credit score.

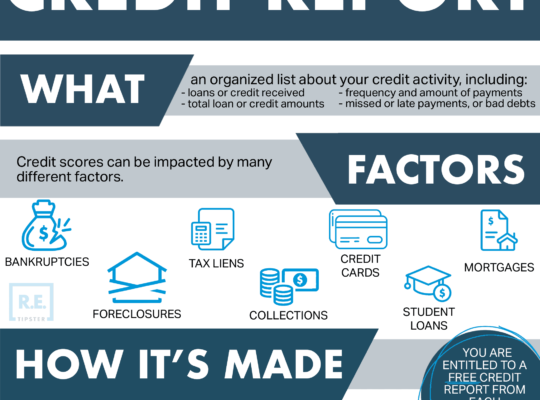

What factors lower a credit score?

There are a number of things that can hurt your credit score. Here are six common factors:

- Missing payments. If you miss payments on a credit card or loan, it will show up on your credit report and negatively affect your score.

- Having too much debt. If you are using too much credit compared to your credit limit, this will raise your debt-to-credit ratio and make you look riskier to lenders. This can also negatively affect your credit score.

- Applying for too many credit cards or loans. Every time you apply for a new credit card or loan, the lender will check your credit report. This is called a "hard inquiry," and it can lower your credit score by a few points.

- Defaulting on a loan. If you stop making payments on a loan and the lender charges it off as a loss, this will seriously damage your credit score.

- Having a short credit history. If you’re just starting to build credit, you may not have enough history for lenders to determine how responsible you are with credit. This can result in a lower credit score.

- Bankruptcy. Filing for bankruptcy will significantly damage your credit score, and the bankruptcy will stay on your credit report for up to ten years.