Back-to-school season or not, credit cards are part of everyday life. But here’s a secret most people miss: when you pay matters almost as much as how much you pay.

The 3 Key Dates to Know

- Statement Closing Date – The date your credit card company totals up your monthly balance. This is what gets reported to the credit bureaus.

- Payment Due Date – When you must pay at least the minimum to avoid late fees.

- Reporting Date – Typically the same as the statement closing date.

Why This Matters

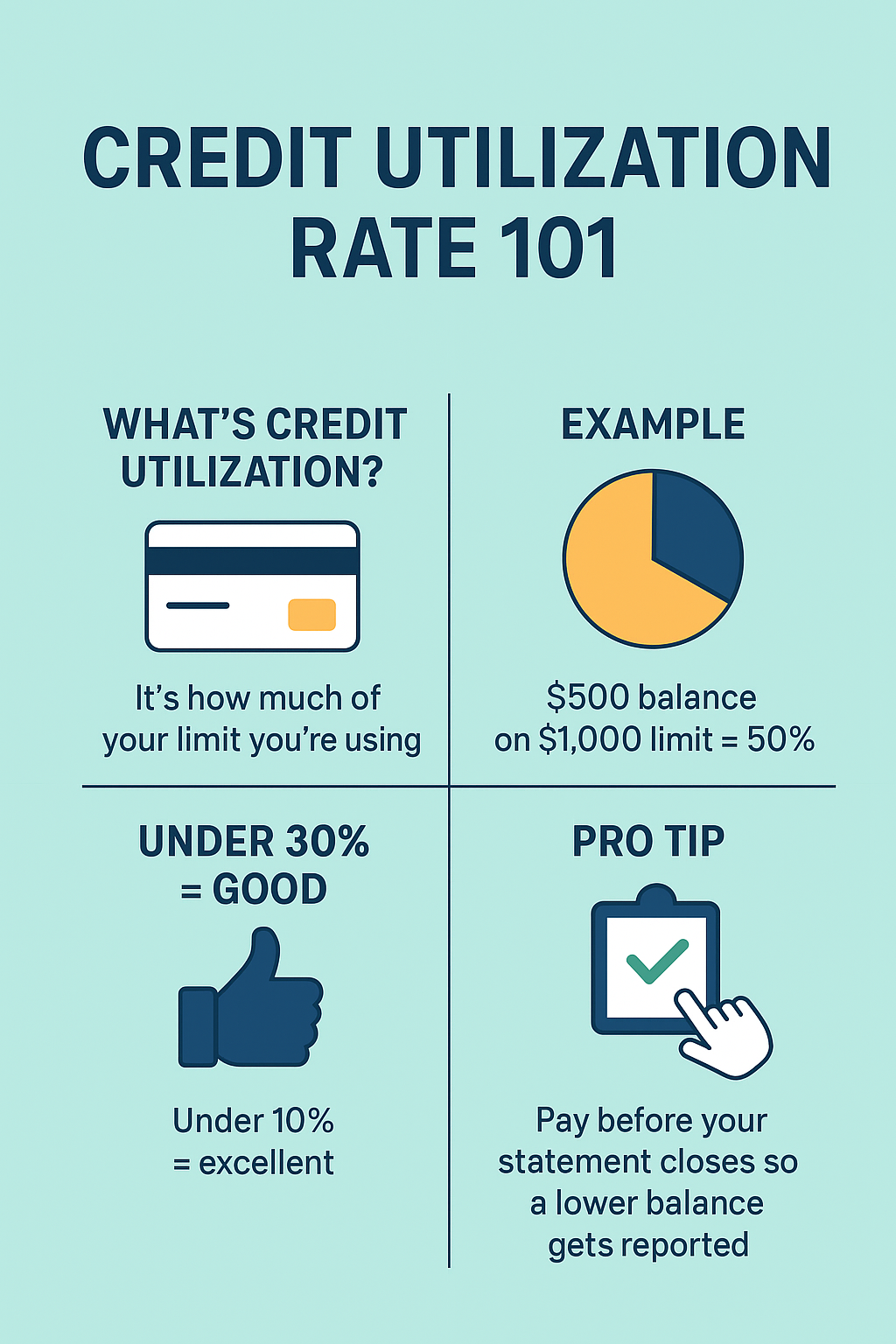

Credit utilization (your balance vs. your credit limit) makes up about 30% of your credit score. Even if you pay in full every month, if you wait until the due date, the bureaus may see a high balance.

Example

- Credit limit: $1,000

- Balance: $600 (60% utilization → hurts your score)

- Pay $500 before statement closing date → reported balance = $100 (10% utilization → much better).

Quick Tips

- Pay twice: once before the statement closing date, and once before the due date.

- Set a calendar reminder or auto-payment to avoid forgetting.

- Use this trick with all your cards to maximize your credit profile.

Bottom line: Paying before your statement closes can make your credit report shine — and help you qualify for better loans, apartments, or even jobs.