Whether you’re just starting your financial journey or trying to recover from past money mistakes, your credit score plays a huge role in shaping your future. From getting approved for a loan to landing a good apartment, understanding how credit works—and how to manage it—is key.

You also might want to read these:

- 7 Credit Card Myths and the Truth Behind Them

- Understanding Credit Scores: 5 Key Factors to Boost Yours

- All About Credit

✅ 1. Why Your Credit Score Really Matters

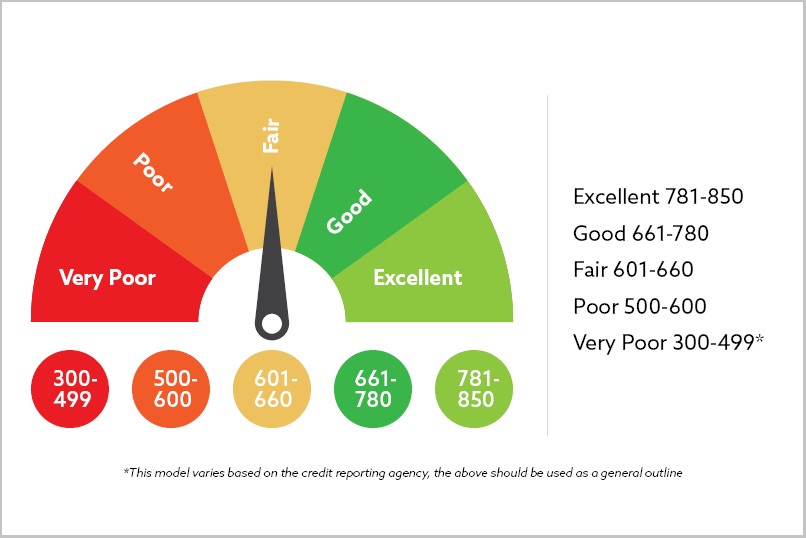

Think of your credit score as your financial reputation. It’s a three-digit number (usually between 300–850) that tells lenders how trustworthy you are with borrowed money.

Here’s what your credit score can affect:

- Loan approvals and interest rates

- Credit card limits

- Rental applications

- Even job applications in some industries

💡 Quick Tip:

A good credit score (typically 700+) can save you thousands in interest over time. That’s money back in your pocket.

Here’s why your credit score really matters:

1. Access to Credit and Favorable Terms:

- Loan and Credit Card Approvals: Lenders, like banks and credit card companies, use your credit score to assess your risk as a borrower. A higher score increases your chances of getting approved for credit products, such as mortgages, auto loans, and credit cards.

- Lower Interest Rates: A good credit score can help you qualify for lower interest rates on loans and credit cards, saving you thousands of dollars over time. Nasdaq reports that with conventional loans, credit scores can impact rates and fees by as much as several percentage points. For example, having a credit score in the 760-850 range for a $300,000 mortgage could result in saving over $116,000 in interest compared to a score in the 620-639 range.

- Negotiation Power: With excellent credit, you might have leverage to negotiate better terms, such as lower security deposits or higher loan limits.

2. Renting an Apartment:

- Tenant Screening: Many landlords and property managers check credit reports during the rental application process to assess your financial reliability and likelihood of paying rent on time.

- Approval and Terms: A good credit score can increase your chances of being approved for a rental and may lead to more favorable lease terms, such as lower security deposits or waived application fees.

- Competitive Markets: In competitive rental markets, a strong credit score can give you an edge over other applicants.

3. Insurance Premiums:

- Risk Assessment: Insurance companies may use credit-based insurance scores to assess your risk and determine your premiums. A good score might lead to lower premiums for auto and home insurance.

- State Restrictions: It’s important to note that some states, like California, Maryland, and Massachusetts, have laws that prohibit using credit to set certain insurance prices.

4. Employment Opportunities:

- Background Checks: Some employers, particularly in sensitive industries like finance and government, may review your credit history as part of their background checks to assess your financial responsibility and trustworthiness.

- Assessing Character: Employers may view a strong credit history as an indicator of reliability and the ability to meet obligations.

- Potential Impact on Job Offers: While not the sole factor, a positive credit report can enhance your employability and increase your chances of getting job offers, especially for positions requiring financial responsibility.

5. Other Financial Services:

- Utility Connections: Some utility companies may check your credit when you apply for service.

- Cell Phone Contracts: Getting a cell phone contract often involves a credit check.

In summary, your credit score is a reflection of your financial habits and plays a vital role in accessing credit, securing rentals, getting favorable insurance rates, and even influencing employment opportunities. It’s essential to understand its significance and take steps to build and maintain a good credit score.

For financial advice, consult a professional. Learn more